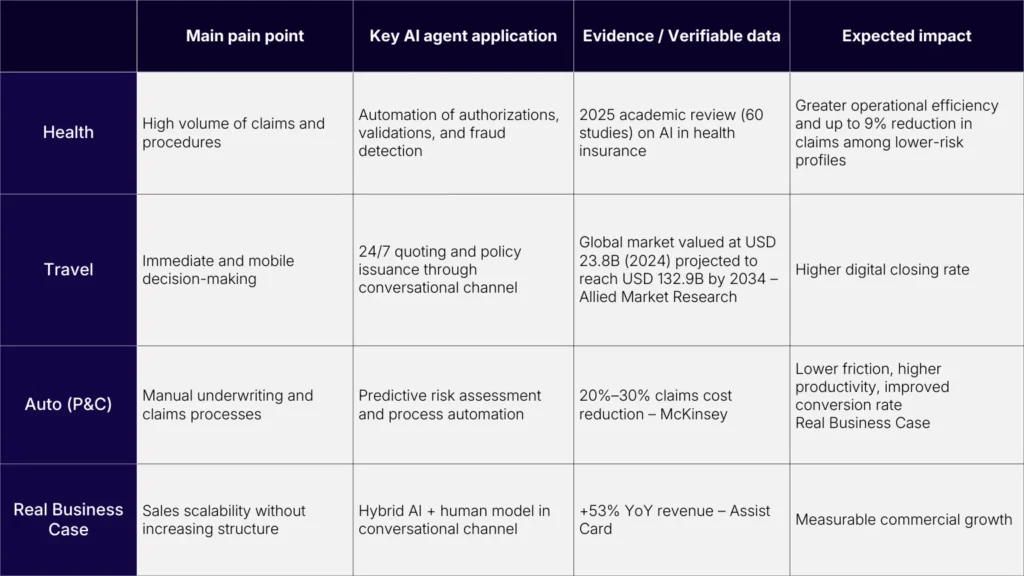

Insurers integrating AI agents into their sales and customer service processes are achieving cost reductions of up to 30%, accelerating policy issuance by more than 40%, and, in specific cases, increasing revenue by over 50%. Health, travel, and auto currently show the greatest impact.

The insurance sector has always competed on price, coverage, and brand. In 2026, it competes on speed, experience, and digital closing capability. The difference between quoting and issuing a policy no longer depends solely on the sales force: it depends on conversational design.

According to the report The future of AI in the insurance industry by McKinsey & Company, intelligent automation can reduce operational costs in insurance companies by between 20% and 30%, especially in back-office and customer service processes. At the same time, Deloitte’s Global insurance outlook 2026 states that the conversation is no longer about experimental pilots, but about executing AI use cases with clear return on investment and controlled risk.

This shows that the debate is no longer whether to use AI, but where it has the greatest impact.

The 53% Figure: When Conversation Becomes Revenue

One of the clearest cases is Assist Card, which, by integrating conversational automation into its digital sales channel, achieved a 53% year-over-year revenue increase under a hybrid model (AI + human support).

Figure 1: Assist Card success case: implementation of a hybrid model (AI + humans) in a conversational channel, with a 53% revenue increase, 27% conversion rate, and 0.7-minute first response time. Source: Chat Center.

The AI agent manages the conversation from first contact, generates real-time quotes, presents options, resolves frequent objections, and sends the payment link. The human team intervenes where consultative value is added or in complex situations.

Result: more closings, less friction, and greater scalability without multiplying structure.

AI in Health Insurance: Efficiency Without Losing Precision

In health insurance, the volume of interactions is massive: authorizations, coverage validations, provider network inquiries, and reimbursements are part of daily operations. Most of these processes follow a structured logic that can be automated.

In this regard, an academic review published in Cost Effectiveness and Resource Allocation (2025) analyzed 60 studies on AI applied to health insurance and concluded that the main impacts are concentrated in predictive pricing, claims management, and fraud detection.

The paper highlights that machine learning-based systems reduce claims processing times by identifying fraudulent patterns and automating reviews, improving operational efficiency and the financial sustainability of the system.

It also mentions scoring and underwriting models based on large datasets that can reduce claim volumes by up to 9% among lower-risk profiles, thanks to better selection and predictive evaluation.

With AI agents integrated into core systems, insurers can:

- Verify coverage in seconds.

- Automate authorization tracking.

- Classify claims before escalating to a human operator.

- Onboard new policyholders without lengthy forms.

The direct consequence is reduced response times and operational relief. The indirect one: greater perceived efficiency from the customer’s perspective.

AI in Travel Insurance: Closing at the Exact Moment

Travel insurance has a distinctive characteristic: the decision is immediate. Users compare, quote, and purchase at the same moment, often from their mobile phones while organizing their trip or even at the airport. There is no room for friction or operational delays.

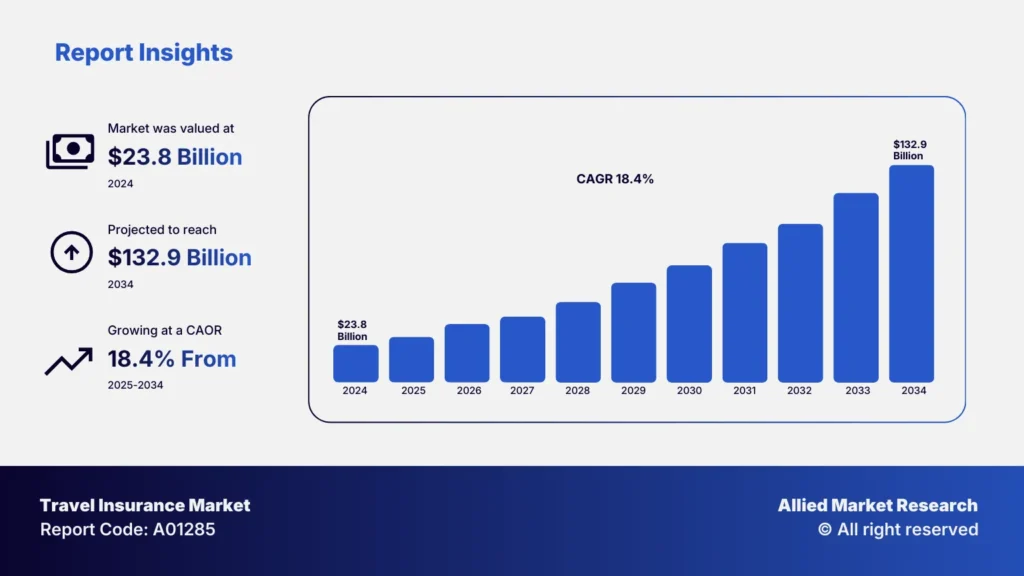

Market growth confirms this dynamic. According to Allied Market Research, the global travel insurance market was valued at USD 23.8 billion in 2024 and is projected to reach USD 132.9 billion by 2034, with a compound annual growth rate (CAGR) of 18.4% between 2025 and 2034. The growth is driven by the sustained recovery of international tourism and the expansion of digital purchasing.

Figure 2: Chart showing projected growth of the global travel insurance market: valued at USD 23.8 billion in 2024, projected to reach USD 132.9 billion in 2034, with a CAGR of 18.4% between 2025 and 2034. Source: Travel Insurance Market Research, Allied Market Research.

In this context, the conversational channel is no longer a complement but a critical closing point. A well-trained AI agent can manage the entire process without human intervention in most cases:

- Generate quotes in seconds based on destination, dates, and traveler age.

- Present clear plan comparisons.

- Suggest relevant upgrades, such as higher medical coverage or extreme sports protection.

- Automatically send the voucher and documentation after payment.

- Recover abandoned quotes through conversational follow-up.

When purchasing is impulsive and the context is mobile, the decisive variable is not just price. It is response speed. In travel insurance, every lost minute is a cooling sale. That is where the AI agent turns a conversation into an issued policy.

AI in Auto Insurance: From Endless Forms to Issuance in Minutes

In auto insurance, the traditional process involves multiple validations: vehicle data, driver profile, claims history, coverage selection, and risk assessment. Every manual friction point not only delays issuance but also increases operational costs.

Industry evidence shows that AI’s impact in this line is tangible. According to McKinsey & Company, in Property & Casualty insurance—where auto insurance is one of the main lines—AI-based automation can reduce claims management costs by between 20% and 30%. Additionally, up to 60–70% of activities in the insurance value chain are technically or partially automatable with current technologies.

In auto insurance, where quote and claims volumes are high and relatively standardized, this automation has a direct effect: less manual intervention, shorter processing times, and faster issuance.

With AI agents connected to the insurance core, the flow can include:

- Structured data collection of vehicle and driver information.

- Real-time predictive risk assessment.

- Automatic generation of multiple quotes.

- Clear comparison of plans within the conversation.

- Payment link delivery and immediate policy activation.

Automation does not eliminate underwriting: it accelerates it. And in auto insurance, where every minute of friction reduces the likelihood of closing, that efficiency directly impacts sales.

In the case of Santander (Autocompara line), optimizing the conversational channel allowed the company to double sales capacity and improve data quality.

Figure 3: Santander Autocompara success case: optimization of the conversational channel with a hybrid model (AI + human support), achieving doubled sales capacity and improved data quality in auto insurance. Source: Chat Center.

Comparative Impact of AI Agents by Insurance Vertical

The implementation of AI agents does not impact all insurance lines in the same way. Health, travel, and auto have different operational dynamics, but in all cases, conversational automation is demonstrating measurable improvements in efficiency, cost reduction, and commercial growth.

From Informational Chatbot to End-to-End Commercial Agent

Digital conversation is no longer a secondary channel in insurance. According to data published by El Economista, nearly half of policyholders already prefer interacting with chatbots over other traditional service channels. This shift is significant: it reflects a transformation in customer expectations, prioritizing immediacy, 24/7 availability, and fast resolution.

At the same time, a report shared by Latino Insurance indicates that digital interactions between insurers and customers have grown by more than 30% in the last two years. The trend is clear: customers are already in digital channels, and conversation volumes continue to increase.

The problem is that many companies still use these channels only to answer frequently asked questions. In 2026, that is insufficient.

The real differentiator is not an informational chatbot, but an AI agent that manages the entire process: from first contact to policy issuance or claim resolution. This implies:

- Automated recovery of abandoned quotes.

- Process management without manual intervention in simple cases.

- Integration with CRM and core systems for real-time operation.

- Commercial scalability without proportionally increasing operational structure.

If nearly half of policyholders already prefer interacting with chatbots and digital interactions are growing at double-digit rates, conversation is no longer support: it is commercial infrastructure.

The difference between responding and selling lies in how that flow is designed. And that is where the AI agent turns every interaction into a measurable result.

Conversational AI: Operational Efficiency with Commercial Impact

Health demands precision. Travel demands speed. Auto demands consultative clarity.

AI agents make it possible to scale these three variables without driving up operational costs. And when well designed—connected to the core, trained on objections, and aligned with commercial objectives—they do not just assist: they sell.

The 53% is not an industry promise. It is a real case. And it demonstrates that conversation, when strategically automated, can turn into revenue.